Does Sequestration Automatically Debar a FAIS Representative?

A representative is sequestrated and the FSP's Key Individual reaches for the debarment paperwork. Stop. The financial soundness pillar in BN 194 does not apply to natural person representatives — which means the three-step chain most people assume (insolvency → financial soundness failure → disqualification) breaks at the first step. Here is what the law actually requires, and why it is structured that way.

By Prepped Editorial

A representative files for provisional sequestration after personal guarantees on a failed

business venture are called up. The FSP's Key Individual calls the compliance officer and asks

whether the representative must be debarred immediately. The compliance officer, who knows that

financial insolvency and financial services regulation are related concerns, pauses. The

instinct to debar is understandable. It is also, on these facts, legally incorrect.

The answer requires working through a specific legislative chain. That chain matters not just

because a real person's career may depend on it, but because RE5 tests it directly — and the

question is designed to catch the candidate who knows the rule well enough to make a confident,

wrong choice.

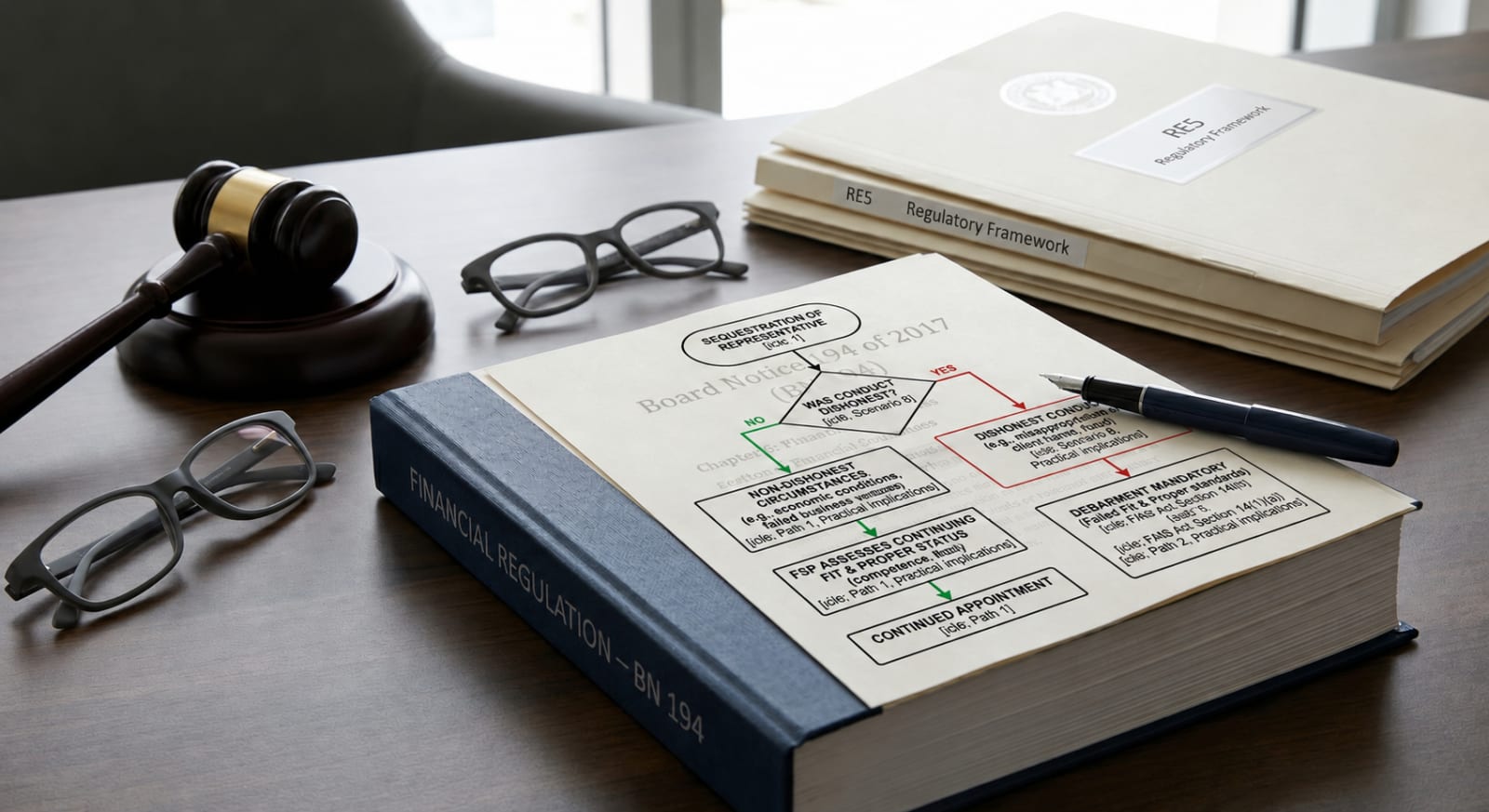

Sequestration Does Not Automatically Debar a FAIS Representative

Sequestration does not automatically debar a natural person representative under the Financial

Advisory and Intermediary Services Act 37 of 2002 (FAIS Act). The financial soundness

requirements in Chapter 6 of Board Notice 194 of 2017 (BN 194) are explicitly disapplied to

key individuals and representatives who are natural persons under Section 43(b)(i). Because

that pillar does not apply to natural persons, insolvency cannot trigger disqualification

through it. The FSP must instead assess the circumstances of the insolvency under the honesty

and integrity framework in Chapter 2 of BN 194, and determine whether the representative

continues to meet the fit and proper requirements under the FSP's ongoing duty in

Section 13(2)(a) of the FAIS Act. The outcome of that

assessment — not the fact of sequestration itself — determines whether continued appointment

is appropriate.

The Legislative Framework

Section 43(b)(i) of BN 194 — Financial Soundness Does Not Apply to Natural Persons

Chapter 6 of BN 194 contains the formal financial soundness requirements: asset-to-liability

ratios, working capital thresholds, and liquidity requirements. Section 43 sets out who these

requirements apply to:

"43. The fit and proper requirements relating to financial soundness contained in this Chapter

(a) subject to paragraph (b), apply to —

(i) all FSPs; and

(ii) juristic representatives;

(b) do not apply to —

(i) a key individual or a representative that is a natural person..."

The exemption is unconditional. It does not depend on whether the representative holds client

funds, handles premiums, or manages any assets. A natural person representative who is

sequestrated has not failed a financial soundness test, because no such test is conducted in

respect of them.

This is the structural foundation of the entire analysis. Once it is understood, the

misconception dissolves.

Section 40(1)(a)(i) of BN 194 — Operational Ability and the Insolvency Restriction

Insolvency does appear in BN 194 in relation to natural person representatives — but in a

different chapter, under a different pillar. Section 40 deals with Operational Ability. It

provides:

"40. (1) An FSP must ensure that where it appoints a person as a representative —

(a) the person —

(i) is not declared insolvent or provisionally insolvent..."

This provision creates a restriction at the point of appointment: the FSP may not appoint

a person who is already declared insolvent or provisionally insolvent. It does not operate as

an automatic termination of an existing appointment. For a representative already in the role

who becomes insolvent, the ongoing obligation to assess continued fitness falls not under

Section 40 itself, but under Section 13(2)(a) of the FAIS Act — the FSP's continuous duty to

be satisfied that its representatives comply with the fit and proper requirements. Section 40

also requires, at appointment, that the appointment must not materially increase risk to the FSP

or to the fair treatment of clients (Section 40(1)(c)), but the enduring assessment obligation

for a currently appointed representative is driven by Section 13(2)(a).

The distinction matters. Section 40(1)(a)(i) is an appointment gateway, not a debarment trigger.

Chapter 2 of BN 194 — Honesty, Integrity and Good Standing

The honesty and integrity pillar, in Sections 7 to 10 of BN 194, applies to all persons

without exception — FSPs, key individuals, and natural person representatives alike. Section 9

sets out what constitutes prima facie evidence that a person does not meet the honesty and

integrity standard. The list includes criminal convictions for theft, fraud, forgery, perjury,

and offences involving dishonesty; civil liability for fraud, misrepresentation, or breach of

fiduciary duty; and related conduct.

Insolvency is not on the list.

This is deliberate. Becoming insolvent is not, by itself, evidence of dishonest conduct.

A representative who becomes insolvent because of economic conditions, illness, or a failed

business venture has not demonstrated the kind of conduct that undermines the trust a client

must place in them. A representative who becomes insolvent because they misappropriated client

premiums to fund personal obligations has demonstrated exactly that — but the trigger for

debarment in that case is the fraudulent conduct, not the insolvency.

Section 10 of BN 194 creates the representative's disclosure obligation:

"10. An FSP and key individual must disclose to the Registrar, and a representative must

disclose to its FSP, promptly and on own initiative, fully and accurately, all information...

which may be relevant in determining whether that person complies or continues to comply with

the requirements relating to honesty, integrity and good standing."

When a representative is sequestrated — provisionally or finally — they must disclose this

to their FSP promptly and on their own initiative. The disclosure runs to the FSP, not to the

FSCA. Section 10 does not specify a fixed number of days; the requirement is prompt and proactive.

Section 13(2)(a) of the FAIS Act — The FSP's Ongoing Duty

The FSP cannot treat the sequestration as the representative's private matter. Section 13(2)(a)

of the FAIS Act imposes a continuous statutory obligation:

"An authorised financial services provider must —

(a) at all times be satisfied that the provider's representatives... are, when rendering a

financial service on behalf of the provider, competent to act, and comply with —

(i) the fit and proper requirements..."

When a representative is sequestrated, this ongoing duty is triggered. The FSP must investigate,

assess, and document. If the FSP allows the representative to continue rendering services without

conducting this assessment, the FSP is potentially in breach of Section 13(2)(a) — regardless

of whether the representative's fit and proper standing is ultimately confirmed.

Section 14(1)(a) of the FAIS Act — When Debarment Becomes Mandatory

Debarment is mandatory under Section 14(1)(a) once — and only once — the FSP is satisfied,

on the basis of available facts and information, that the representative no longer meets the fit

and proper requirements or has materially contravened the FAIS Act. The obligation reads "must

debar," not "may debar." But the trigger is the FSP's satisfaction after assessment, not the

occurrence of any specified event including sequestration.

Where Representatives and FSPs Go Wrong

The intuitive chain runs as follows: insolvency means financial distress; financial distress

means financial unsoundness; financial unsoundness means failure of the financial soundness

pillar; failure of the financial soundness pillar means disqualification. Three logical steps,

each of which feels reasonable.

The chain breaks at step one. Financial soundness is a genuine pillar of the fit and proper

framework — it applies to FSPs and juristic representatives, and for those entities, Section

44(3) of BN 194 imposes a hard prohibition: an FSP or juristic representative may not continue

as such if declared insolvent, even provisionally. The legislature created that hard rule

deliberately. But it simultaneously, and equally deliberately, excluded natural persons from

Chapter 6 entirely. The financial soundness pillar was designed for entities, which bear capital

adequacy obligations. It was not designed to assess the character of individuals. That is

Chapter 2's function.

Because financial soundness is a real pillar with real consequences for entities, it is easy to

assume it applies universally. It does not.

The Section 11 confusion is a separate and equally common error. Section 11(1)(a)(ii) of

the FAIS Act provides that a licence lapses where the licensee, being a natural person, is

finally sequestrated. This creates an automatic, conclusive consequence — but it applies to

the FSP licence held by a natural person (a sole proprietor who is themselves the FSP), not to

a representative's authority to render financial services. Representatives do not hold licences.

They operate under the FSP's licence. Section 11 has no application to the question of whether

a natural person representative may continue after sequestration.

The two provisions — Section 11 (licence lapsing for a sole proprietor FSP) and Section 14

(debarment of a representative) — describe different legal mechanisms with different triggers

and different subjects. Conflating them is one of the errors the RE5 examination is specifically

constructed to catch.

How This Works in Practice

Scenario A: Provisional sequestration, no dishonesty involved

A financial planner working as a representative for a Category I FSP is placed under provisional

sequestration. Personal guarantees on a failed property development were called up; the

sequestration resulted from a lawful commercial risk. He immediately discloses the provisional

sequestration to his FSP, as required by Section 10 of BN 194.

The FSP must now assess two things. First, under Chapter 2 of BN 194: does the conduct that

led to the sequestration reflect dishonesty or a lack of integrity? On these facts, the answer

is no — the circumstances involve commercial failure, not fraudulent conduct. The representative

is not prima facie dishonest under Section 9(1). Second, under the FSP's ongoing duty in

Section 13(2)(a) of the FAIS Act, read with the fit and proper requirements in BN 194: does

continuing his appointment materially increase risk to the FSP or to the fair treatment of

clients? If satisfied on both counts that the answer is no, the FSP may allow him to continue

rendering financial services.

The FSP should document this assessment. The absence of documentation, not the sequestration

itself, creates the compliance risk.

Scenario B: Sequestration arising from misappropriation of client funds

A short-term insurance representative is provisionally sequestrated after it emerges that he

systematically withheld client premiums rather than paying them over to the insurer. The

insolvency was caused directly by that conduct.

The FSP's Chapter 2 assessment reaches a different conclusion. The conduct underlying the

insolvency — systematic misappropriation of client premiums — falls squarely within Section

9(1)(a)(ii) of BN 194: theft, fraud, or an offence involving dishonesty. The FSP is satisfied,

on available facts and information, that the representative no longer meets the honesty and

integrity requirements. Debarment under Section 14(1)(a) is mandatory.

The distinction between these two scenarios is not the fact of insolvency. Both representatives

are insolvent. The distinction is the conduct that caused it.

Practical Implications

For FSPs and Key Individuals

When a representative discloses a sequestration (or the FSP becomes aware of one through other

means), the obligation is to assess, not to assume. The assessment focuses on two questions:

Does the conduct underlying the insolvency reflect dishonesty or a lack of integrity under

Chapter 2 of BN 194? Does continuing the appointment materially increase risk to the FSP or

to clients — assessed under the FSP's ongoing duty in Section 13(2)(a) of the FAIS Act, read

with the fit and proper requirements in BN 194? Document the assessment and its findings. If the

assessment concludes the fit and proper requirements are no longer met, debarment is mandatory

under Section 14(1)(a) of the FAIS Act and cannot be deferred.

For Representatives

Provisional or final sequestration does not automatically end your appointment. The obligation

that attaches immediately is disclosure to your FSP under Section 10 of BN 194 — prompt,

proactive, and full. Your FSP will conduct an assessment. The relevant question is not whether

you are financially distressed, but whether the circumstances of that distress reflect conduct

incompatible with the honesty and integrity standard. If the sequestration arose from

circumstances involving no dishonest conduct, your fit and proper standing under Chapter 2 is

not compromised. If it did involve dishonest conduct, the debarment risk exists because of that

conduct, not because of the insolvency itself.

If debarment does occur, the path back to the industry is governed by Board Notice 82 of 2003,

which sets out the reappointment requirements including a minimum 12-month waiting period from

the debarment date, resolution of all unconcluded client business, and full compliance with

fit and proper requirements at the time of reappointment.

For Exam Candidates

When you see a sequestration scenario in the RE5 examination, the key question to ask before

looking at the options is: which fit and proper pillar is actually at issue here? For a natural

person representative, financial soundness is never the answer. The analysis runs through

Chapter 2 (honesty and integrity) and the FSP's ongoing assessment duty under Section 13(2)(a)

of the FAIS Act. Section 40(1)(a)(i) governs the point of appointment only — it does not

operate as a termination trigger. The answer that describes an automatic disqualification is

almost certainly wrong; the answer that describes a required assessment is almost certainly right.

Put this into practice

Turn insight into preparation

If you are preparing for RE exams or building a stronger prep pipeline for your team, Prepped helps you move from theory into deliberate practice.

Try for FreeKeep exploring

Related insights

Can You Tell a Client You Filed a Suspicious Transaction Report?

A representative files a Suspicious Transaction Report and tells the client what was reported. The impulse is understandable - but the act is a criminal offence under Section 29(3) of FICA, carrying a maximum penalty of 15 years' imprisonment. Here is what the law actually requires, and why the instinct to be transparent is precisely the wrong response.

When Must a FAIS Representative File a Cash Threshold Report — and What Counts as "Cash"?

A client walks in and hands over R55,000 in cash. Most financial advisers know a Cash Threshold Report is required — but not how quickly, not whether the transaction must stop, and not whether that travellers' cheque counts as "cash" under the Act. The answers are in Section 28 of FICA, and they are more specific than most practitioners realise.

What Is the FAIS Ombud's Jurisdictional Limit — and What Happens When Your Claim Exceeds It?

A client with a R4.2 million loss wants to use the FAIS Ombud. The Ombud's jurisdictional limit is R3,500,000. The client assumes the Ombud is not available. That assumption is wrong — but only if the client understands and agrees to the abandonment mechanism. Here is how the jurisdictional limit works and what the decision to abandon actually means.